Is your universal life insurance collapsing?

Here is what happens.

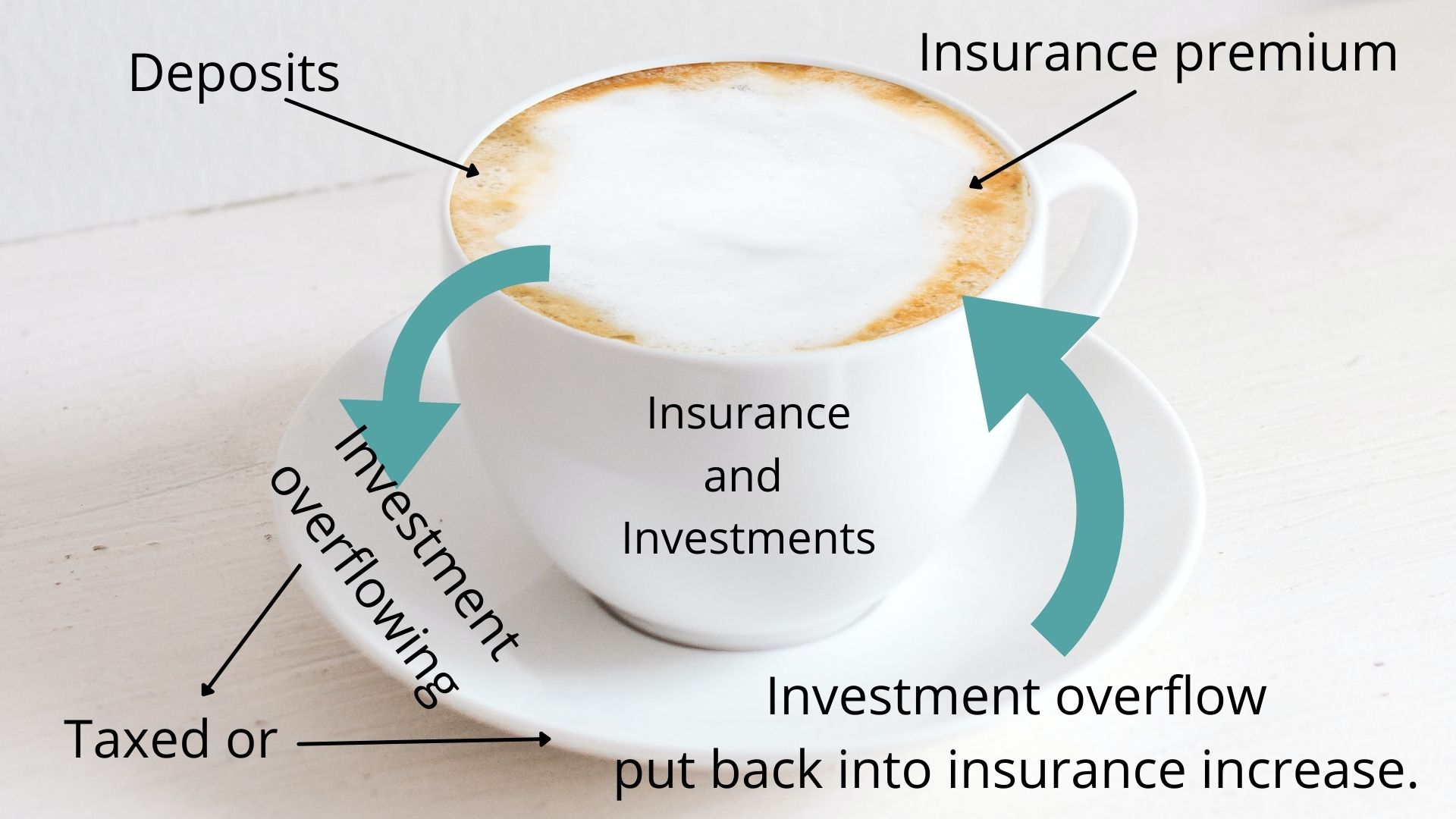

You pay a premium each month into the policy. Wrapped up in that policy premium are a few things, the cost of insurance (taxes, administrative, and covering the death benefit) and savings/investments.

What happens for many is that each year the cost of insurance goes up. Because you are paying only the minimum premium to keep the policy in force, at some point, the cash value(or lower death benefit) is going to have to be used to help pay the premium. That is not always bad, depending on your goals.

If the investments are not growing, you risk the collapse of the policy. For example, a daily interest account is simply not going to increase the account. At some point, you are not going to be able to make the premium payment. That means you have to dump some money into it, or lower the death benefit, or surrender the policy, or it collapses. Either way, you are going to lose.

Universal life insurance can be a great product, especially if you are young enough to take advantage of time. However, there is a shelf life on the policy, and you need to make sure it is set up correctly?

Questions to ask about your Universal life policy when you review?

1)When you look at the original illustration that was shown to you. What was the estimated investment return? Sometimes, some will inflate that number to an unrealistic return.

2)When you look at the original illustration that was shown to you. How long before it starts taking away from your investment and is going the wrong way?

3)When did you last speak with the life insurance agent? You should be checking in each year for a review?

4)What type of investments are you invested in, or is it just a daily savings account? Those are low, low returns, by the way.

5)What is the purpose of the life insurance policy you have? This determines the type of product you need.

6)Do you have any cash value? Do you understand what the cash value can be used for?

So what questions do you have?

Want a review of where you are at and your policy? Take the no-obligation complimentary financial analysis.