Understanding Universal life insurance

Universal life insurance brings together permanent insurance with a tax-advantaged investing with some limits.

Premium

In UL policies, four things make up the premium, and you get to see each of those costs. They are mortality cost, investment returns and expenses and premium tax(all the premium is taxed).

Premium Payment options

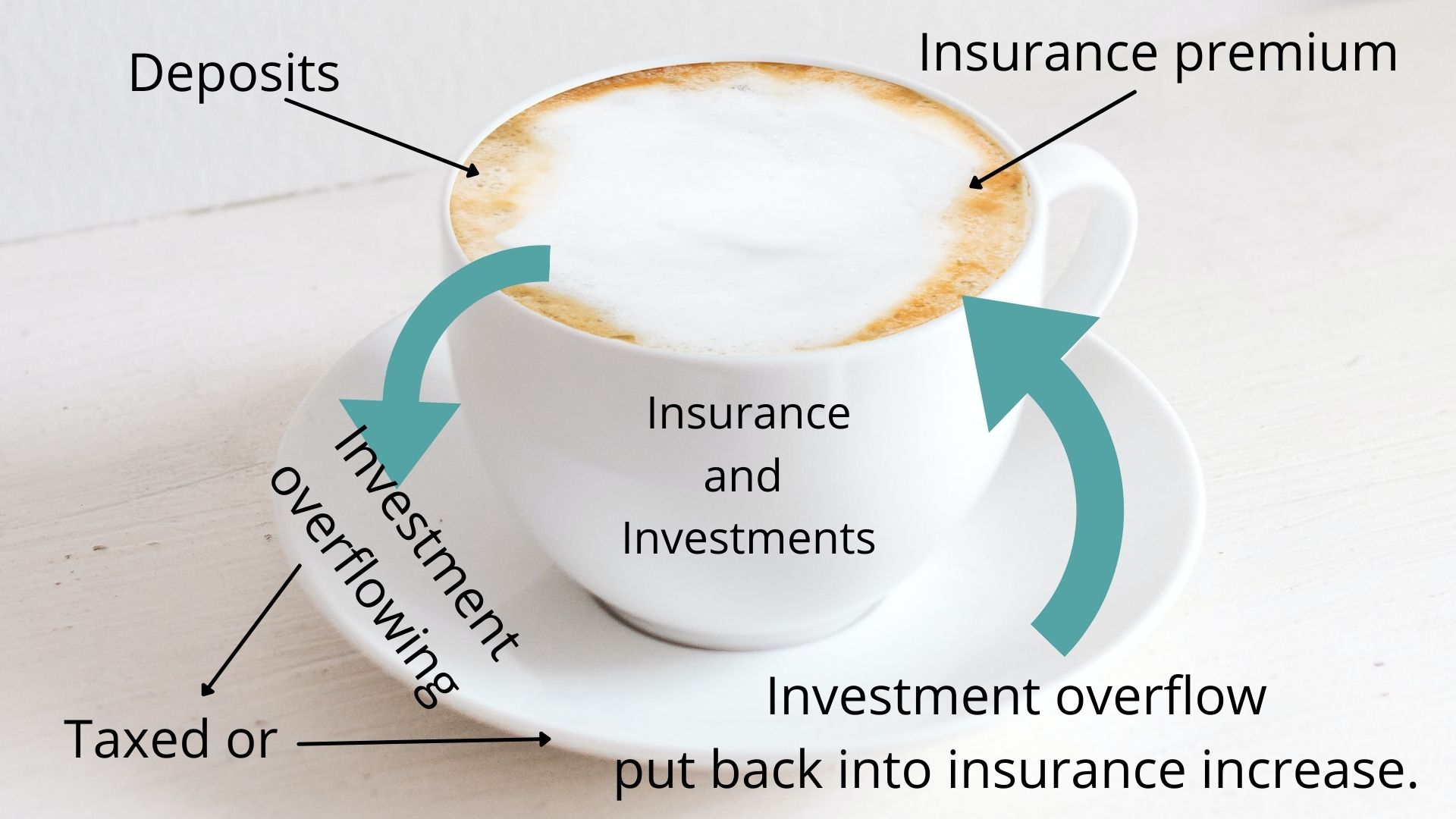

The policyholder has some room to decided how much to pay in premiums and when to pay them. There is a minimum premium that covers the cost of the policy and keeps a policy operation. However, there is not enough in the minimum premium to build the investment account. Thus you will need to increase your premium to invest. One can increase what they pay or lower it in the future.

Often there is a max amount paid on the premium to ensure that one stays within the tax-exempt status. It is not recommended, but you could stop paying the premium, assuming there is enough in the investment account to cover the cost. Over time, however, your account will decrease.

To help stay in the tax-exempt status, insurance companies will put the overflow investment into increasing the insurance. Other wise you will have to pay tax on the investments that reach a certain level.

Investments of UL

When you pay your premium, and after-tax, and cost are taken out, the rest is invested by the insurance company. This investment is tax-sheltered; however, there is a limit here. Due to the fact that this is an insurance policy and an investment, there is a limit on the tax-sheltered part. There is the potential of paying tax if you exceed the limit.

There is a wide range of investment options, and one would need to select what best meets their goals.

Yearly renewable term (YRT) or level cost of insurance costing(LCOI)

The difference is that yearly renewal term cost changes each year, and the level cost of insurance does not over the years. The YRT will be lower in the early years and the cost of insurance, but the morality cost will later increase and eat at the investment.

The LCOI will have less money to invest early, but the morality cost will not be as high in the later years. Deciding which one is for you will depend upon your goals.

Death Benefit options

a)Level death benefit

The benefit will stay the same from the original face amount or equal to the policy’s account value when it goes over the original face amount. This type will cost less and be useful if you do not need to increase your insurance needs over time.

b)Level death benefit plus account value

The mortality deductions will be more significant; however, the beneficiary will get the original amount of insurance and the account value.

c)Level death benefit and cumulative premiums

Here you get the death benefit plus the premiums paid over the time of the contract. There will be a cost increase for this. It needs to be noted that if the account value is more than the original face amount and total premiums, that excess is kept by the insurance company.

d)Indexed death benefit

The death benefit is indexed for inflation.

How much insurance should I get?

This depends on your needs and wants and income. The best place to start is with the complimentary financial analysis. This provides a great review of needs, wants and where you are at.

In short Universal life insurance is permanent insurance with an investment option that can provide a tax shelter.

What questions do you have?

You may be interested in this post also https://matthewlaker.com/is-your-universal-life-insurance-collapsing/

Why wait? Let’s meet and start with a Free Financial Analysis and get you a solution to protect your family and leave a legacy.